DeFi yield-farming — a process of locking up crypto assets in return for token rewards — exploded over the summer as millions of dollars flowed into all kinds of protocols, but the market quickly cooled off when the ultra-high yields disappeared in September. After the bubble burst, many top DeFi token prices posted heavy losses the following month.

However, partly due to the surge in the price of BTC and to the anticipation for the launch of Phase 0 of Ethereum 2.0 on Dec. 1, the optimism around DeFi has been recovering — and so have the prices of DeFi tokens.

Meanwhile, centralized exchanges like OKEx have also played an important role in improving the popularity of DeFi projects, since many exchanges have been quick to list new DeFi tokens. According to OKEx’s August Microstructure Report, DeFi tokens accounted for only 19% of OKEx’s total spot trading volume. This number jumped to 25% in September.

With data provided by blockchain analytics firm Kaiko, OKEx Insights analyzed multiple DeFi tokens traded on centralized exchanges in an effort to provide market participants with a different perspective on the changing appetites for such tokens over time. The 10 tokens examined were:

Balancer (BAL)

Compound (COMP)

Curve (CRV)

Kyber Network (KNC)

Chainlink (LINK)

SUN

SushiSwap (SUSHI)

Uniswap (UNI)

yearn.finance (YFI)

DFI.money (YFII)

The DeFi cycle, at a glance

Some of the most important events to have transpired in the DeFi sector this year include:

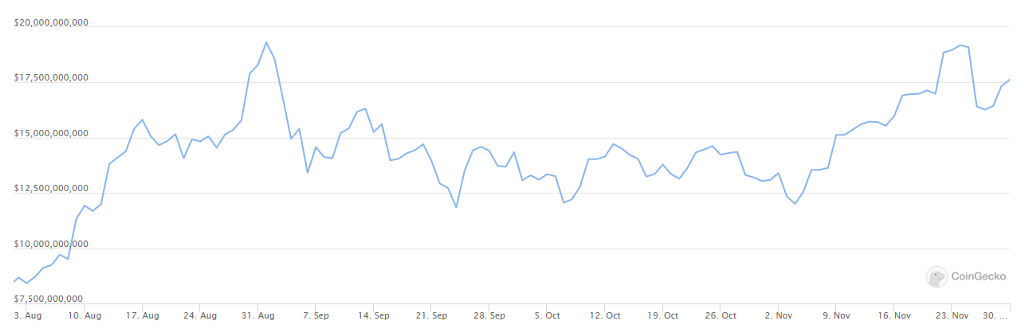

The total value locked in decentralized — which simply indicates the aggregate amount of capital stored in DeFi smart contracts — surged from $1 billion in early July to $9.75 billion at the start of September, which was the peak of the nascent market’s explosion. On Sept. 2, Ethereum transaction fees were pushed to an all-time high of, on average, 0.032 ETH per transaction (worth around $15, at the time). The TVL in DeFi then saw its largest retracement, falling from the high of $9.75 billion to $7.79 billion in the span of only four days in early September.

The migration away from DeFi protocols in September came at a time when both traditional and cryptocurrency markets were hit hard. This translated to a sell-off of DeFi tokens, which pushed their prices down even further. However, the total value locked has resumed rising since then, with various twists and turns. Likewise, the sum of all DeFi projects’ market capitalization has generally been on the rise in November — though, this figure still hasn’t recovered from its Sept. 2 all-time high of $19.55 billion.

With the price of BTC plummeting nearly 10%, from $11,500 to $10,000, on Sept. 3, it was not surprising that the DeFi bubble would finally burst. Ultra-high yields became extinct following the plunge of token prices, and yield-farming returns gradually fell back to a range more in line with their high-risk levels. BTC regained $11,500 after 40 days, but DeFi tokens generally experienced a long decline and did not rebound until early November.

Trading volumes reveal changing preferences of exchange users

The DeFi boom over the summer and early fall made users of centralized exchanges eager to build or hedge their DeFi exposures. By the end of September, OKEx had listed 50 DeFi tokens on the platform, offering coin-margined swaps for eight of these DeFi tokens and USDT-margined swaps for 27 of them — although some swaps did not launch in time to catch the peak in late August and early September.

OKEx Insights examined 10 high-volume DeFi token swaps using data from Kaiko. The volume of swaps shows that exchange users’ appetite for trading newly created DeFi tokens and yield-farming tokens has been enthusiastic, to say the least.

Prior to September, DeFi’s long-time leader by market capitalization, LINK, dominated up to 80% of the trading volume of the 10 tokens selected. The arrival of a SUSHI perpetual swap on OKEx started to eat away at a portion of LINK’s dominance. By Sept. 6, SUSHI’s perpetual swap trading volume had surged to $10 million, taking a 10% share away from LINK’s dominance. Further growth in DeFi trading volume continued over the following week, with the swap trading volumes of YFII and YFI reaching $51 million and $28 million, respectively, by Sept. 12. As a result, LINK’s trading volume dropped rapidly, with its dominance falling below 25%.

The listing of a UNI perpetual swap on OKEx was the next highlight of September, which drove a significant increase in trading volume on the exchange. UNI saw a massive $183 million in perpetual swap volume on the second day of trading, accounting for 70% of the intraday volume of the 10 selected tokens — a huge difference from the market enthusiasm for SUSHI. UNI’s popularity was maintained until mid-October, when trading volume was flipped again by LINK and, subsequently, traders’ enthusiasm for UNI rapidly declined.

Additionally, we observed that overall DeFi swap volumes dropped precipitously in the second half of October due to the persistent decline in DeFi token prices, YFI and YFII gained a greater share of the overall volume, due to their tremendous volatility. YFI, for example, fell from a high of $40,000 to $8,000 in approximately 50 days. During this downturn, market participants moved away from trading DeFi tokens.

The bottoming out of prices for these new DeFi tokens began on Nov. 5, when the price of BTC rose from $14,000 to nearly $16,000. The price of UNI recovered 14% on that date, after dipping to as low as $1.80. Since then, the prices of DeFi tokens have followed BTC’s dramatic rise and many of them outperformed BTC in November.

In terms of swap trading volume, LINK’s percentage of the total DeFi volume once again declined — YFI, for example, rebounded from $15 million on Nov. 1 to $97 million on Nov. 18. Other DeFi tokens, meanwhile, also showed a significant increase in swap trading volume.

When examining the volumes illustrated above, one outlier we see is that Nov. 7, which was an extremely heavy trading day — with YFI, YFII and LINK volumes at their highest levels in two and a half months. This coincided with the day that Joe Biden became president-elect, as per widespread consensus, in the United States. This event triggered a trading boom on centralized exchanges that wasn’t seen on decentralized exchanges such as Uniswap. YFI made a particularly volatile move that day, rising from $11,800 to a high of $17,500 before closing around $14,000. At that same time, however, BTC fell nearly 5% intraday, with a 9% price swing.

Another interesting observation is that one week before Uniswap ended its first phase of liquidity mining on Nov. 17, SUSHI’s volume grew rapidly. The average daily volume for SUSHI after Nov. 12 jumped from less than $10 million to more than $20 million, showing that market participants saw the ending of UNI rewards as a positive event for SUSHI. When it comes to decentralized exchanges, this sentiment is more clearly reflected in the changes of TVL in DeFi — i.e., liquidity providers transferred their funds from Uniswap to SushiSwap or other yield-farming projects.

Visit https://www.okex.com/ for the full report.

OKEx Insights presents market analyses, in-depth features, original research & curated news from crypto professionals.

Not an OKEx trader? Sign up, start trading and earn 10USDT reward today!

was originally published in OKEx Blog on Medium, where people are continuing the conversation by highlighting and responding to this story.